Before you decide what happens to the house, find out what will actually work.

In divorce, the home is the largest asset, and the mortgage is usually the last thing anyone checks. We help you know, before you sign, whether you can keep it, refinance it, or need a different plan.

Book your free Strategy Review →20 minutes. Confidential. No cost, no card, no sales pitch. Conducted by a CDLP®.

The most overlooked mistake in divorce

The house is the largest asset. The mortgage is the last thing evaluated.

Settlement agreements don't fail on paper. They fail in execution — months later, when a lender's underwriting guidelines don't match what was negotiated. By then, the options have narrowed.

A spouse is awarded a home that they ultimately can't refinance.

Support income doesn't qualify the way it was assumed.

Equity is divided without modeling the financing impact.

Future homeownership is unknowingly compromised.

If the mortgage doesn’t work… the settlement doesn’t work.

Book a free consult if any of this sounds familiar.

- You've been told you can keep the home, but you're not sure if it actually works.

- You're trying to make decisions without complete financial clarity.

- You don't know how support, debt, or equity will affect your options.

- You're divorcing and own real property, and refinance may be required.

- You want clarity before signing — not after.

The Divorce Mortgage Planning Report™

Not a loan estimate. Not a pre-qualification. A structured analytical roadmap built by a Certified Divorce Lending Professional (CDLP®) using the four-phase Mortgage Capacity Mapping™ framework — the same report your attorney, mediator, and financial neutral can use in mediation, drafting, and litigation.

Property Feasibility Analysis™

Income Qualification Structuring™

Debt Allocation Impact Modeling™

Equity & Cash Flow Solutions Engineering™

Divorce law is different in every state.

Your guidance should be too.

Whether you're in a community property state or an equitable distribution state changes how the home and the mortgage get divided. Pick your state for guidance built around your local rules, lender environment, and tax quirks — or browse all 50.

Jody Bruns has spent more than 25 years at the intersection of divorce, real estate, and mortgage finance. After watching too many divorces fall apart financially in the months and years after settlements were signed — not because the legal work was wrong, but because no one had checked whether the housing decisions actually worked under real lending rules — she founded the Divorce Lending Association and created the Certified Divorce Lending Professional® (CDLP®) designation. That framework now supports professionals nationwide. But every piece of it still comes back to one question: will this actually work for the person who has to live with it?

Read more about Jody

The Risk Isn't the House. It's the Unverified Plan.

In divorce, settlement agreements often allocate the home to one spouse.

But a court order does not guarantee mortgage qualification.

Refinance timelines. Debt reassignment. Support income. Title transfer.

These legal decisions must align with lending standards, or financial strain follows.

Mortgage capacity is not awarded in a divorce. It must be evaluated.

Don't wait until after the agreement to find out it doesn't work. Once settlement decisions are made, your options become limited.

Book My Free CDLP® Strategy ReviewNot ready for a call? Start with the 60-minute Divorce Housing Strategy Roadmap™ - a guided self-paced experience covering the financial and mortgage considerations most divorces miss.

Start with the Divorce Housing Strategy Roadmap™"I came in convinced I could keep the house. The roadmap walked me through why I couldn't — at least not the way the settlement was being written. I would rather have learned that for $47 than for $47,000 a year from now."

— Sarah M., metro Atlanta

"I went into mediation with real numbers instead of hopes. That alone changed everything. I stopped agreeing to things I didn't fully understand and started asking the questions I should have been asking from day one."

— Lauren K., Phoenix

"I was about to sign off on a buyout that would have wrecked my ability to refinance later. Sixty minutes of structured questions caught it. I'm not great at math and not great at finance — this made it make sense."

— David R., Raleigh, NC

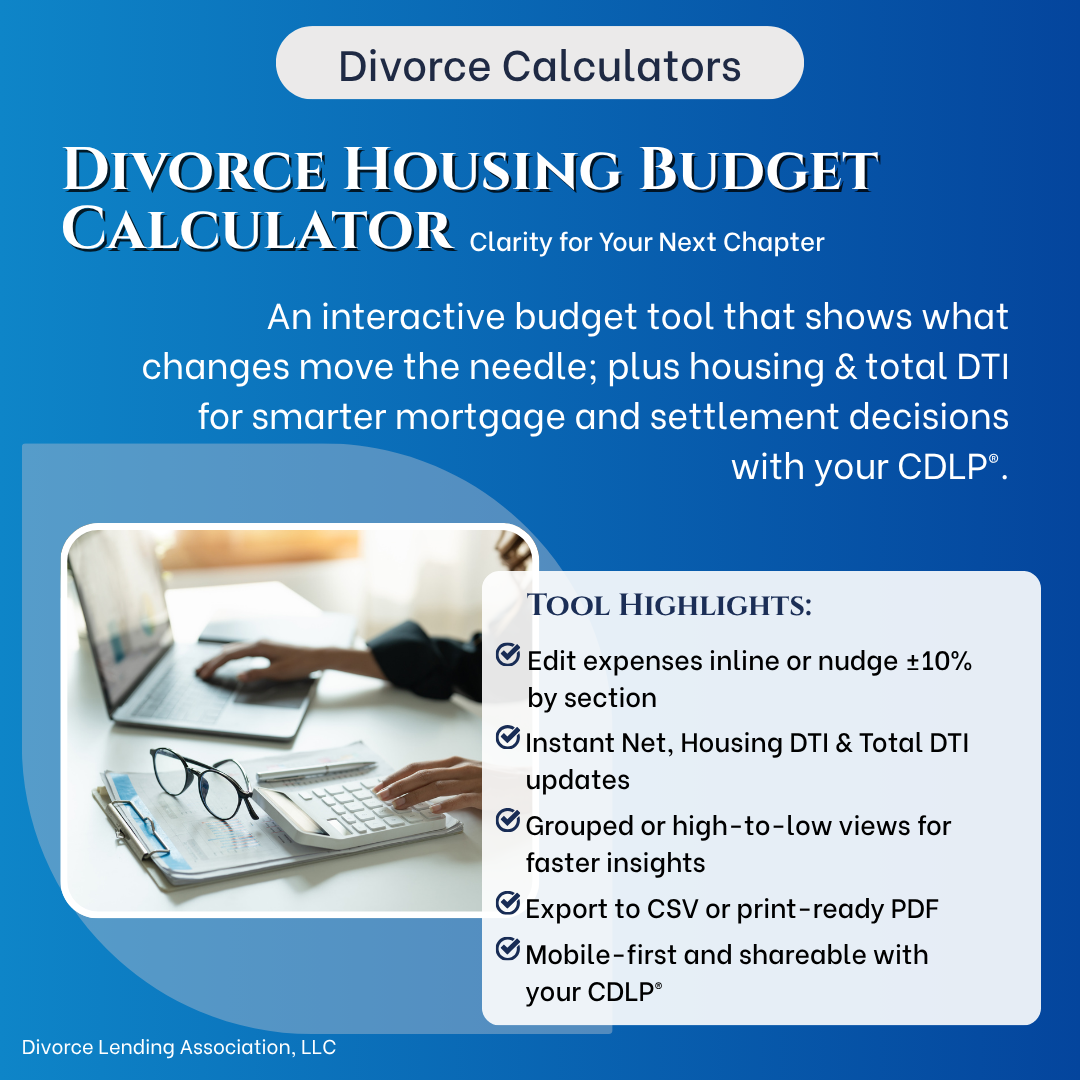

Start Organizing Your Numbers

Use the Housing Budget Builder to understand how income and expenses may interact after divorce.

Build Your Housing Budget

Built Within the Divorce Lending Association

Used by Certified Divorce Lending Professionals Nationwide.

Divorce Housing Strategy operates as a division of the Divorce Lending Association — aligning legal, financial, and housing evaluation principles used by divorce-focused professionals nationwide.

Housing decisions during divorce require coordination across multiple disciplines. No single professional governs them all.

This framework was built to introduce structure before legal commitments are finalized.

The structured evaluation principles introduced here reflect the same framework relied upon by Certified Divorce Lending Professionals nationwide.

The attorney, mediator, or financial neutral on your team can train on this same framework through The Alignment Series™ — continuing education (CLE, CME, CE, CJE) from the Divorce Lending Association. Learn more ›

Divorce Lending Association | Certified Divorce Lending Professional (CDLP®) | Mortgage Capacity Mapping™

Learn About the Divorce Lending AssociationFrequently Asked Questions About Divorce Housing Decisions

Housing decisions during divorce often involve legal, financial, and lending considerations that do not naturally align. These questions address some of the most common areas of confusion.

What happens to the house in divorce?

Can I keep the house after divorce?

What is a Divorce Housing Strategy Session™?

When should I schedule a Free Consultation?

Do I need a mortgage professional during the divorce process?

What happens after the Free Consultation?

Before You Decide What to Do With the House…

Real guidance for real decisions. Explore expert insights on navigating the marital home, understanding your mortgage options, and making informed housing decisions before, during, and after divorce. These aren’t just articles; they’re strategies designed to protect your future.

Your Divorce Mortgage Planning Report

5 Mistakes Divorcing Couples Make

Can (Should) I Keep the House in a Divorce?

Can I Assume The Mortgage in a Divorce?

Free download

Not ready to talk yet? Start with the free checklist.

Get the Divorce Real Estate & Mortgage Checklist, the same first step our experts use, so you know what to gather and what to ask before any decision is final.

No spam. Just the checklist and occasional guidance. Unsubscribe anytime.